Issue, No.37 (March 2026)

How Pension Systems (Re)shape the Landscape of Wealth Inequality and Redistribution

Disclaimer: This article is based on a longer research paper, “Welfare states and wealth inequality: Pension systems, the public-private mix, and augmented wealth in old age” – a joint work with Javier Olivera (LISER) and Philippe Van Kerm (University of Luxembourg).

Key Messages

- Pensions play a strong redistributive role in shaping wealth distribution: estimated wealth inequality when pension entitlements are included is between 15 and 40 percent lower across countries than marketable wealth inequality alone.

- When pension entitlements are counted as wealth, the cross-national patterning of wealth inequality changes significantly and resembles that of income inequality.

- The relative size of pension systems matters more than the progressivity of benefit design: large-scale pension systems tend to compress the overall wealth distribution by limiting the outsized influence of marketable wealth, which is typically far more unequally distributed.

Introduction

Wealth inequality has increasingly been recognized as one of the most pressing social problems of our time. Research shows that wealth inequality has been continuously rising across high-income countries since the 1980s (Piketty & Saez, 2014). Higher levels of wealth inequality tend to undermine equality of opportunity and intergenerational mobility (Beckert, 2022). Extreme concentrations of wealth can also weaken democratic governance, as top wealth holders may exercise disproportionate political influence (Page et al., 2013).

One of the common findings from the academic literature is that wealth inequality has distinct features and dynamics compared to income inequality. Across countries, wealth inequality is only weakly correlated with income inequality (Pfeffer & Waitkus, 2021). For example, Nordic countries that are known to be the most equal societies in terms of income distribution display high levels of wealth inequality, comparable to those in the United States (US), a country known for having the highest level of income inequality among advanced economies.

Most empirical studies on wealth inequality count only ‘marketable wealth’ – financial assets, real estates and other real assets – in their wealth measurement, excluding pensions and other social insurance entitlements. However, this approach can substantially understate households’ available economic resources, given that individuals with access to generous social benefits are less likely to accumulate large savings to insure themselves against future income risks. Moreover, the scale and design of welfare states vary hugely across countries, implying that cross-national comparisons of wealth inequality without considering social insurance entitlements may present a distorted picture.

Against this background, our study examines the redistributive role of pension systems by estimating wealth inequality when pension entitlements are translated into wealth values. Admittedly, pensions represent just one part of the welfare state – the institutional configuration of social policies, including benefits for families, unemployment, sickness, healthcare, and so on – but still account for the largest share of social expenditures. To offer relevant policy implications, we further explore the institutional features that explain cross-national differences in the redistributive power of pension wealth.

How much do pension systems redistribute wealth?

We used the Luxembourg Wealth Study (LWS) Database (LIS Cross-National Data Center, 2025), combined with the Wittgenstein Centre’s Human Capital Database (KC et al., 2024), to estimate the wealth value of household pension entitlements. Based on the latter database, we first computed gender-, education-, and cohort-specific remaining life expectancy at each age for all countries. The resulting life expectancy dataset was then merged with the LWS sample of older households in 17 high-income countries. The wealth value of pensions was obtained from calculations assuming that current pension incomes are received over the remaining lifetime until death, while survivors’ pensions are received from after a partner’s death. Using this simulated wealth of pension entitlements, we can evaluate the redistributive impact of pension systems by computing the percentage difference between ‘augmented’ and ‘marketable’ wealth inequality – the Gini coefficients of household wealth including and excluding pension wealth, respectively.

We also classified country-specific pension systems into three regimes – Comprehensive, Basic Security, and Hybrid types. Comprehensive systems are represented by most continental and Southern European countries, as well as by Finland, where large, dominant public pension schemes provide earnings-related benefits financed on a pay-as-you-go basis. In these countries, the role of private pensions is limited as the public system offers relatively generous income replacement rates even for high-income retirees. In contrast, in basic security systems the main public pillar focuses on minimum income provision through flat-rate benefits regardless of previous earnings or contributions. Therefore, large private pension markets are developed in these countries. Finally, hybrid systems feature an earnings-related public system but with significantly lower replacement rates for higher-income retirees. Private pensions therefore play an important role mostly for the upper and middle classes, although in Estonia private pillars remain relatively underdeveloped due to rapid structural transformation.

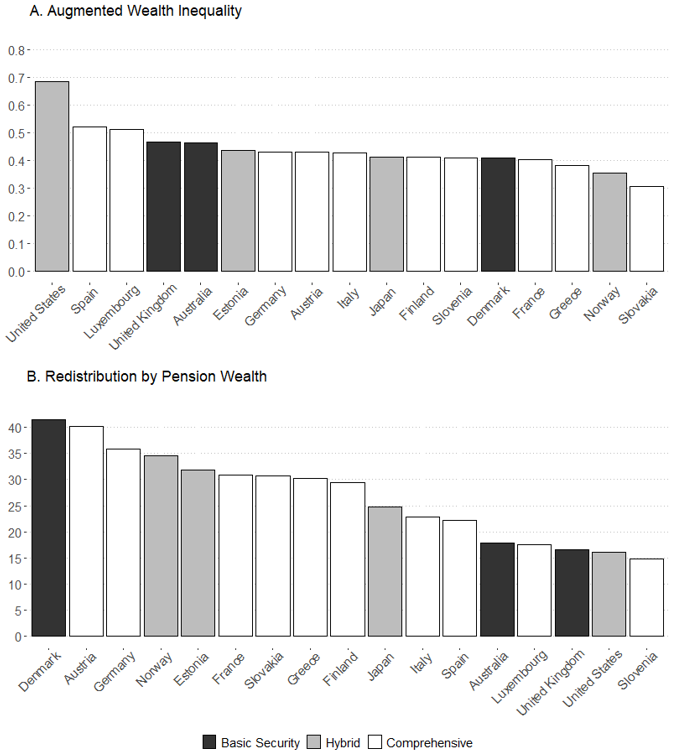

Figure 1. Augmented Wealth Inequality (A) and Redistribution by Pension Wealth (B)

Figure 1A shows the level of augmented wealth inequality measured by the Gini coefficient across countries, whereas Figure 1B illustrates the percentage difference between marketable and augmented wealth inequality. Overall, wealth inequality looks much smaller when pension wealth is taken into account, ranging between 0.30 and 0.52 for most countries, except for the US – an extreme outlier. This is considerably lower than marketable wealth inequality that ranges between 0.5 and 0.85. Redistribution through pension wealth is particularly large in Denmark, Austria, Germany, and Norway, where wealth inequality declines by nearly or over 35 percent when pension wealth is considered. On the other hand, in Australia, Luxembourg, the United Kingdom (UK) and the US, the achieved wealth redistribution is below 20 percent, and in Slovenia it is as low as 15 percent.

Such huge variation in the redistributive power of pension wealth reshuffles the cross-country ranking of wealth inequality. When only marketable wealth inequality is considered, measured wealth inequality is among the highest in Austria (0.72), Denmark (0.70), and Germany (0.67), but these countries move to the middle or lower end of the cross-country distribution once pension wealth is included. By contrast, Luxembourg, the UK, and Australia rank around the middle in terms of marketable wealth inequality but move closer to the top in augmented wealth inequality.

Is wealth inequality so different from income inequality?

As noted earlier, an important insight from the literature is that income and wealth follow distinct dynamics. The former is a flow at specific points in time, whereas the latter is a stock that accumulates over time. As a result, income and wealth inequalities do not always correspond to each other. There are many workers with high salaries but hold relatively few assets. Conversely, most older households have lower incomes than working-age households but may still possess substantial wealth.

At the country level, the correlation between income inequality and (marketable) wealth inequality is known to be weak (Pfeffer & Waitkus, 2021). However, this picture is likely incomplete because wealth inequality is compared across countries with highly different pension systems. Older adults tend to hold less marketable wealth when public pension systems guarantee generous income streams in retirement. Moreover, private defined-contribution pensions are sometimes captured as household wealth, but public pension entitlements are not. Evidence also suggests that there is an inverse relationship between public pension spending and home ownership rates across countries (Dewilde & Raeymaeckers, 2008).

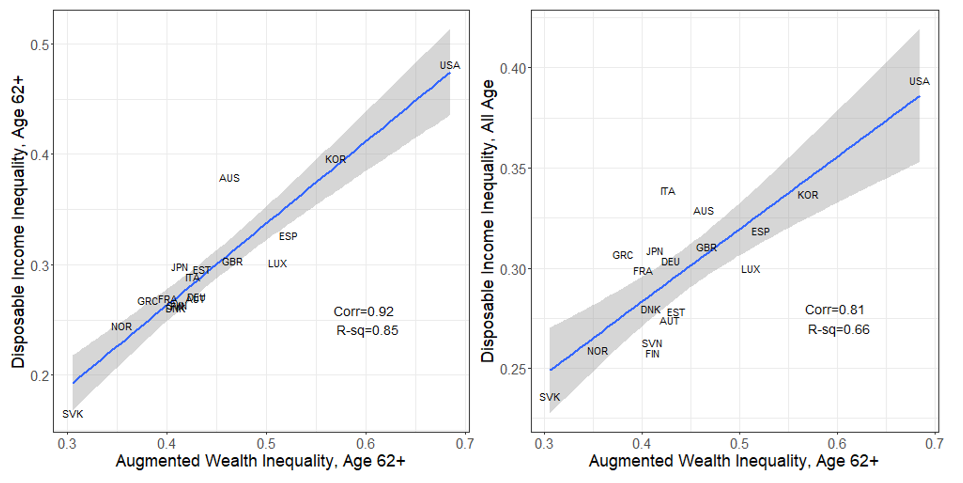

Figure 2. Augmented wealth inequality in old age versus disposable income inequality in old age (left) and versus disposable income inequality in the total population (right)

Figure 2 presents the cross-country correlation between augmented wealth inequality – the same measure shown in Figure 1A – and household income inequality, also based on the LWS sample. The left-hand-side panel of Figure 2 shows that, when pension systems are considered, wealth inequality and income inequality are strongly correlated, with a Pearson correlation of 0.92. One might argue that this relationship is merely tautological, since augmented household wealth is partly derived from household pension income. To address this problem, the right-hand-side panel of Figure 2 uses household income inequality measured for the entire population rather than only among older households. The correlation is still high at 0.82.

The importance of the institutional pension design

Then what explains the large cross-national variation in the redistributive power of pension wealth? To explore the role of institutional pension designs, we conducted a decomposition analysis by classifying household wealth into four components: financial wealth, real wealth, public pension wealth, and private pension wealth. We decomposed the relative contributions of public and private pension wealth to overall inequality into two elements: (a) the share of pension wealth in total augmented wealth (relative size); and (b) the concentration coefficient – the degree to which pension wealth is concentrated at the top or bottom of the augmented wealth distribution. Using the concentration coefficient, we can capture how progressive pension systems are: the more pension wealth is concentrated toward the bottom, the more progressive the pension system.

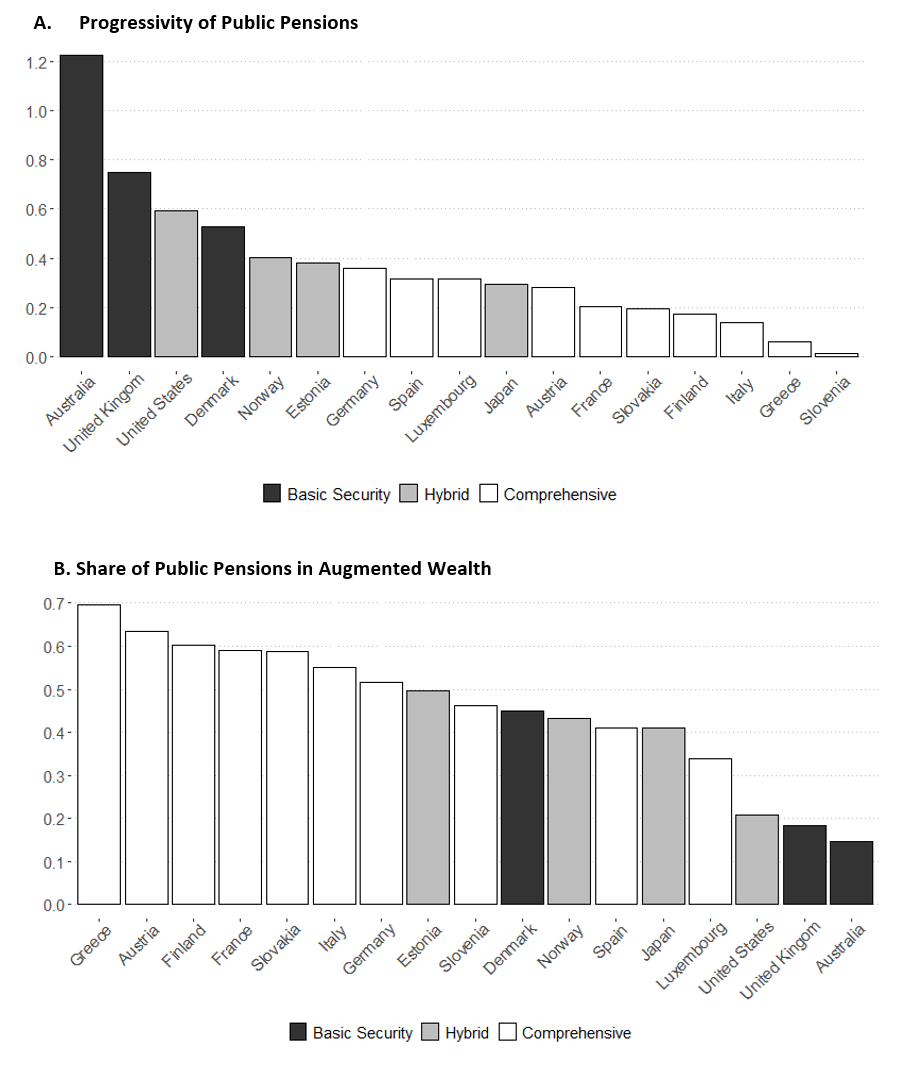

Figure 3. Progressivity Index (A) and Share (B) of Public Pension Wealth

Figure 3A displays the progressivity index of public pension systems across the selected countries. Consistent with the pension regime classification, public schemes in basic security countries are the most progressive by institutional design, followed by hybrid countries except for Japan. Comprehensive public systems, by contrast, show less progressive structures. On the other hand, the share of public pension wealth in total wealth, as shown in Figure 3B, is generally higher in comprehensive countries than in basic security countries, while hybrid countries do not show a consistent pattern within the group.

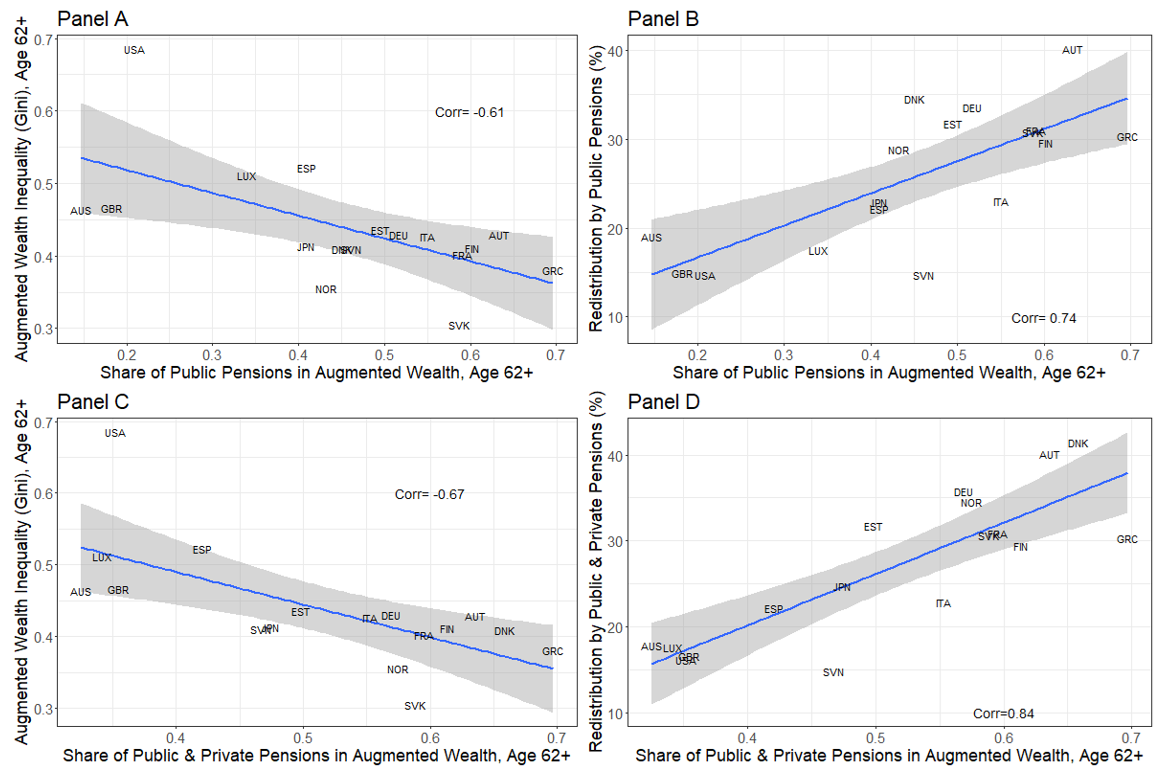

Figure 4. Share of Public Pensions (Panels A, B) and Public & Private Pensions (Panels C, D) versus Wealth Inequality (Panels A, C) and Redistribution (Panels B, D)

Figure 4 reveals that, rather than the progressivity of the benefit design itself, it is the share of pension wealth (its relative size) that is strongly associated with the redistributive power of pension systems – and overall wealth inequality. Countries where pension wealth accounts for a larger share of total wealth tend to achieve greater redistribution through pension systems. The relationship is stronger when both public and private pension wealth are considered compared to when solely public pension wealth is included. Countries with more progressive pension designs often achieve relatively weak redistribution through pension systems, largely due to its smaller share of pension wealth in total wealth.

Concluding remarks

For most households – maybe except for the super-rich – pensions are an important source of economic well-being and a substitute for personal savings, despite their limited market exchangeability and liquidity. Our analysis shows that pension systems play a massive redistributive role in shaping wealth inequality. When household pension entitlements are translated into wealth values, wealth inequality looks significantly lower in all countries, by around 15 to over 40 percent, compared to when only counting marketable wealth. The redistributive impact depends strongly on the size of pension wealth relative to other forms of wealth within a country. The result implies that large-scale pension systems may crowd out the influence of other wealth sources, such as financial and housing assets, which tend to be much more unequal than the distribution of (earnings-related) pension entitlements.

Another important finding is that the mix of public and private pensions better predicts wealth inequality and redistribution through pensions than public pensions alone. While it is commonly assumed that private pension schemes mainly benefit high-income retirees more and are thus less redistributive, in several cases including Denmark, Norway, and the UK, private pensions are an important source of wealth for middle- and even low-income households. This challenges the simple dichotomy of public and private pensions. The way private pension schemes work is highly context-dependent, and their impact may be contingent on how they are managed, collectively organized, and regulated.

References

| Beckert, J. (2022). Durable Wealth: Institutions, Mechanisms, and Practices of Wealth Perpetuation. Annual Review of Sociology, 48(1), 233–255. https://doi.org/10.1146/annurev-soc-030320-115024 |

| Dewilde, C., & Raeymaeckers, P. (2008). The trade-off between home-ownership and pensions: Individual and institutional determinants of old-age poverty. Ageing and Society, 28(6), 805–830. https://doi.org/10.1017/S0144686X08007277 |

| KC, S., Dhakad, M., Potancokova, M., Adhikari, S., Yildiz, D., Mamolo, M., Sobotka, T., Zeman, K., Abel, G., Lutz, W., & Goujon, A. (2024). Updating the Shared Socioeconomic Pathways (SSPs) Global Population and Human Capital Projections (WP-24-003). International Institute for Applied Systems Analysis. |

| LIS Cross-National Data Center. (2025). Luxembourg Wealth Study (LWS) Database [multiple countries]. http://www.lisdatacenter.org |

| Page, B. I., Bartels, L. M., & Seawright, J. (2013). Democracy and the Policy Preferences of Wealthy Americans. Perspectives on Politics, 11(1), 51–73. https://doi.org/10.1017/S153759271200360X |

| Pfeffer, F. T., & Waitkus, N. (2021). The Wealth Inequality of Nations. American Sociological Review, 86(4), 567–602. https://doi.org/10.1177/00031224211027800 |

| Piketty, T., & Saez, E. (2014). Inequality in the long run. Science, 344(6186), 838–843. |