Issue, No.27 (September 2023)

Impact of the 2018 fiscal reform on wage income in Romania

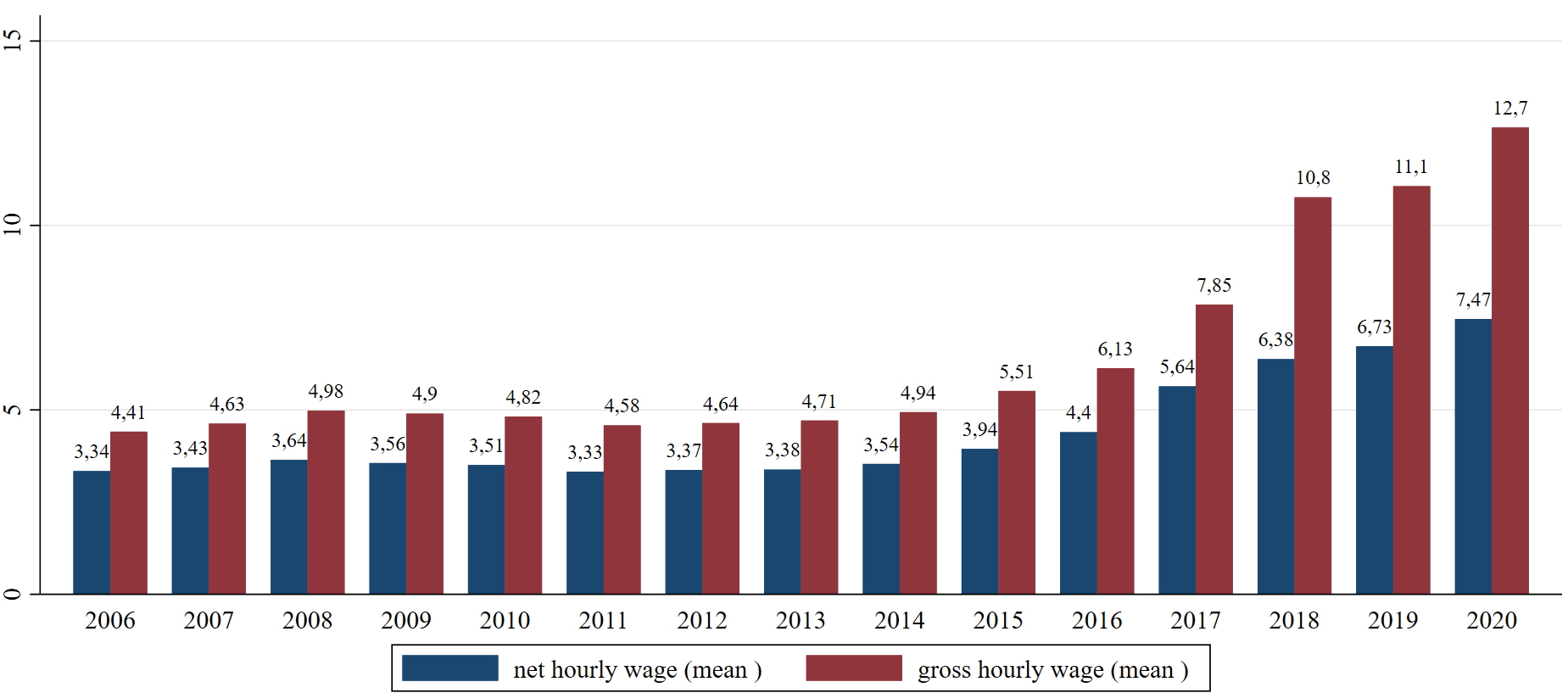

Looking at the newly released long series of Romania in the LIS database, we can observe a remarkable increase in the gross wage income, especially between 2017 and 2018. However, as one can see from Figure 1 below, this steep increase of 37.57 percentage points in hourly gross wages (expressed in purchasing power parity (PPP) rates in order to account for the overtime inflation) is not followed by a similar rise in the net wages (which increased only by 13.12 percentage points during the same period). One of the explanations is the impact of the fiscal reform that was implemented in Romania starting in January 2018 and which shifted most of the social security contributions burden from the employers to the employees. Previously, the employer was paying 22.75% in social contributions for each of his employees and the employees were paying 16% of their gross wages as social security contributions. With the 2018 reform, the contributions paid by the employer decreased to only 2.25%, reducing their labour cost, while the difference is found in the increase to 35% of their gross wages paid directly by the employees as social security contributions. Additionally, the social security contribution was introduced for part-time workers in August 2017. Also in 2017, the maximum ceiling for the calculation base of the compulsory contributions to the pension and health insurance funds was abolished. Although there was no legal obligation to raise the gross wage as a part of the fiscal reform as in other countries, most employers did so through negotiations with their employees. Consequently, the gross wages increased progressively in the next years in order to compensate for this substantial rise in contributions for the employees. This is reflected in the data, and we observe that by 2020 the gross wages increase by an impressive 61.78 percentage points compared to 2017, while the net wages increased only by 32.44 percentage points in the same period. The difference is accounting for the increased burden of the social security contributions for the employees.

Fig.1: Evolution of gross versus net hourly wage over time: Romania 2006-2020

Note: the gross/net hourly wage rate was calculated from the yearly gross/net employee cash or near cash income using information on weekly hours worked; it is limited to those who worked the entire year full time and had only one job at the time of the survey; expressed in PPPs.

Source: own calculations using Luxembourg Income Study (LIS) Database, except for the 2014, 2016 & 2020 datapoints which are based on own calculations using EU-SILC. These datapoints, which are centered around the income reference year, correspond to the 2015, 2017 & 2021 EU-SILC surveys.

For the same period, reflecting the fiscal reform, the variable that measures social security contributions (together with income taxes at the household level in the LIS data) more than doubled in value.

In conclusion, the spectacular increase in gross labour income in the last years in Romania should be regarded with caution, being mostly the reflection of the fiscal reform, which does not translate into a similar increase in disposable (net) wages.

References

| Ban, C., Buciu, P. (2023). Reforma fiscală: propuneri pe termen scurt. https://library.fes.de/pdf-files/bueros/bukarest/20416.pdf |

| IMF Country Report (2018), Romania selected issues, No. 18/149. https://www.imf.org/en/Publications/CR/Issues/2018/06/06/Romania-Selected-Issues-45944 |

| World Bank (2023). Report on the tax system in Romania, including benchmarking and recommendations to inform Client’s reform of the tax framework. https://mfinante.gov.ro/documents/35673/8180698/ReformingthetaxsysteminRomania_BM.pdf |