Issue, No.9 (March 2019)

Extending behavioral variables in the Luxembourg Wealth Study (LWS) Database: what kind of research can be done?

Besides standard socio-economic determinants (e.g. economic resources, age profile, education, gender, etc.) that have been highlighted in the literature as important factors impacting household financial decision-making, research has now turned to an analysis of the importance of behavioral aspects that could affect household financial outcomes. To keep up with the current research trends in the field of household and personal finance, the Luxembourg Income Study (LIS) Data Center will extend the standard set of behavioral variables already present in the Luxembourg Wealth Study (LWS) Database. These behavioral variables cover information on risk aversion, savings behavior, financial literacy, financial planning, as well as several behavioral variables related to debt.

Some of these variables – predominantly focused on risk aversion – have been recently utilized in several LWS research papers (see, Kaliciak et al., 2016; Schneider et al., 2017; Barasinska and Schäfer, 2018). For example, Kaliciak et al. (2016) analyze the relationship between behavioral variables and voluntary retirement savings in Greece, Italy, the UK, and the US, highlighting the importance of financial risk aversion. Barasinska and Schäfer (2018) explored the impact of varying risk preferences across gender on stock market participation.

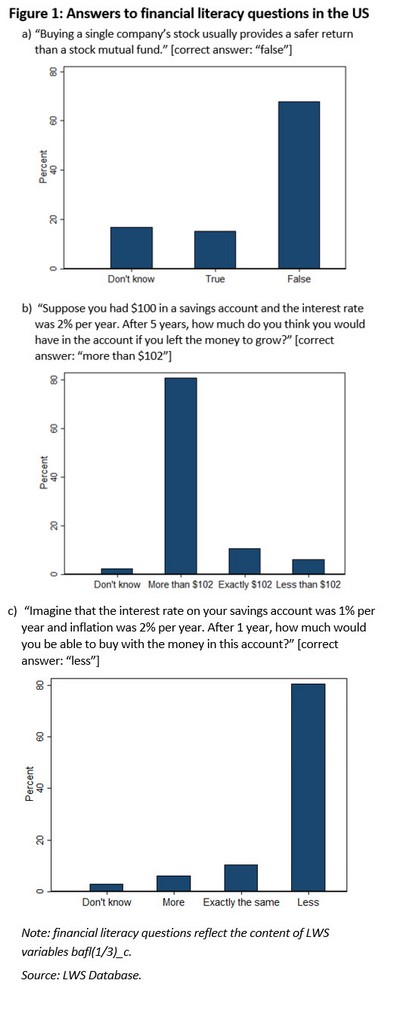

Financial literacy questions asked in the wealth surveys – and also covered in the LWS Database (e.g. Italy, the UK, and the US) – typically follow the standard questions on interest rates, inflation, and risk diversification proposed by Lusardi and Mitchell (2014). For example, the Survey of Consumer Finances (SCF) 2016 asks U.S. households three questions about financial matters (see Figure 1 for the exact wording). The answers to those questions reveal that respondents are more familiar with the concepts of inflation and interest rates than the concept of risk. Following the recent literature, researchers might be interested in linking financial literacy to financial behaviors and economic decisions such as asset holdings, retirement savings, portfolio diversification, as well as over-indebtedness (see Lusardi and Mitchell, 2014), or studying differences in financial literacy across population groups (e.g. Cupak et al., 2018).

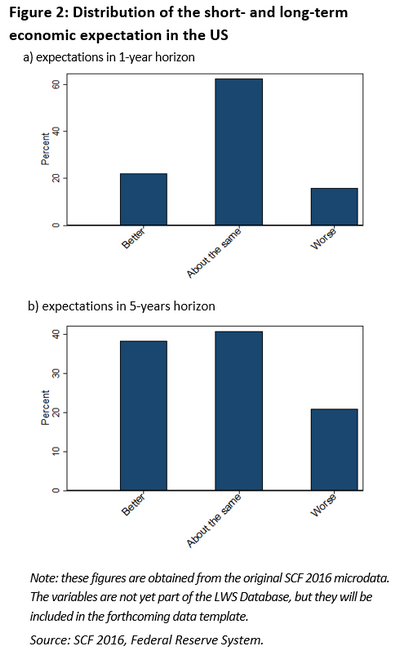

New behavioral variables in the LWS Database on expectations will be based on a set of questions recently asked in several wealth surveys. Typically, there are two different sets of questions asked with respect to expectations, the overall performance of the economy (e.g. economic growth and prices) and expectations regarding the future financial situation of the household. Let us take a look at some examples from the original questions that will appear as new LWS variables. For example, in the SCF 2016, the following questions are asked: “Over the next five years, do you expect the U.S. economy as a whole to perform better, worse, or about the same as it has over the past five years?” and “Over the next year, do you expect the economy to perform better, worse, or about the same as now?”. As shown in Figure 2, households in the US have different expectations regarding future macroeconomic trends.

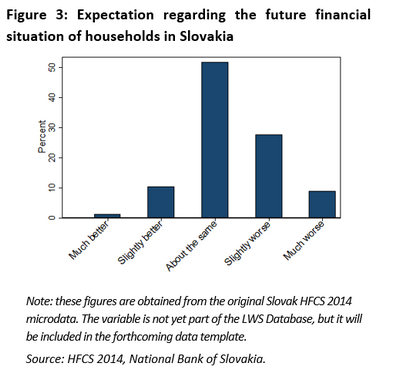

Another wealth survey (the Household Finance and Consumption Survey) asks a question about households’ expectations concerning their future financial situation: “Thinking about a year from now, do you expect your personal financial situation in general to be a lot better, somewhat better, about the same, somewhat worse, or a lot worse?”. The answer to this question is presented in Figure 3. In a sample of Slovak households, respondents showed mostly neutral, but also rather pessimistic expectations as regards the evolution of their future financial situation.

From a research perspective, household expectations play an important role in determining economic behaviors such as life-cycle consumption (e.g. Jappelli and Pistaferri, 2000) or choosing an optimal level of debt (e.g. Brown et al., 2005). The forthcoming LWS expectation variables could be utilized by researchers in a similar manner.

It is important to stress that currently the cross-country availability of the above-discussed behavioral variables is limited in the LWS Database, since the wealth surveys have only recently begun to collect such data. In line with the current developments in empirical research on household and personal finance, we hope that more wealth surveys will continue to collect behavioral variables and that they will therefore appear more frequently in the LWS for researchers to conduct cross-country analyses.

References

| Barasinska, N. and Schäfer, D. (2018). Gender role asymmetry and stock market participation – evidence from four European household surveys. The European Journal of Finance, 24(12), 1026–1046. |

| Brown, S., Garino, G., Taylor, K., and Price, S. W. (2005). Debt and Financial Expectations: An Individual‐ and Household‐Level Analysis. Economic Inquiry, 43(1), 100-120. |

| Cupak, A., Fessler, P., Schneebaum, A., and Silgoner, M. (2018). Decomposing gender gaps in financial literacy: New international evidence. Economics Letters, 168, 102-106. |

| Jappelli, T. and Pistaferri, L. (2000). Using Subjective Income Expectations to Test for Excess Sensitivity of Consumption to Predicted Income Growth. European Economic Review, 44(2), 2000, 337-358. |

| Kaliciak, A., Kurach, R., and Merouani, W. (2016). Who is Eager to Save for Retirement–the Cross-Country Evidence. LIS WP (No. 23). LIS Cross-National Data Center in Luxembourg. |

| Lusardi, A., and Mitchell, O. S. (2014). The economic importance of financial literacy: Theory and evidence. Journal of Economic Literature, 52(1), 5–44. |

| Schneider, C. R., Fehrenbacher, D. D., and Weber, E. U. (2017). Catch me if I fall: Cross-national differences in willingness to take financial risks as a function of social and state ‘cushioning’. International Business Review, 26(6), 1023–1033. |